One of the biggest reasons why economic events such as hyperinflation are so devastating is because they occur in a flash, and usually beyond the reach of governments and central banks to be able to stop them. And in a nutshell, the invisible hand of market forces will always outdo anything man can construct to oppose them, just as nature will always win out over technology in the long run.

And now we are seeing these market forces begin to rebel against the ZIRP and NIRP policies implemented by the central banks as the interbank lending rate, or LIBOR, is now rising at an ever accelerating clip despite the ‘controls’ put forth by the financial masters of the universe.

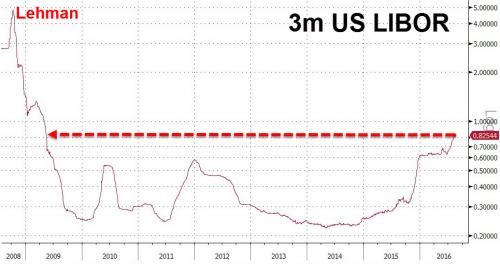

Even while most interest rates are falling, a key short-term rate is rising fast. The three-month London interbank offered rate, or Libor, has climbed to 0.82% from 0.67% a month ago and 0.33% a year ago. It now stands at a seven-year high.

Higher Libor rates increase funding costs for banks and loan payments for individuals and companies that have adjustable-rate loans indexed to Libor. That includes most business loans, home-equity loans, adjustable mortgages, and private student loans, as well as some car loans.

Add in all of the securities derived from bundles of these loans, and the total impact of rising Libor reaches into the trillions, estimates Pimco. - Barrons

Think of the dichotomy now taking place between Libor and Negative Interest Rates (NIRP), which create the opposite effects for central banks who need rock bottom rates to coax businesses and consumers to keep spending. Ie… rises in Libor will make borrowing for the general economy much higher at the same time the Fed, ECB, and Bank of Japan need an environment of low rates to sustain their massive bubbles.

And speaking of Japan, they are already becoming victim to the Libor rates accelerating rise.

So far US banks have escaped largely unscathed, but the higher funding costs and shrunken market are hitting Japanese banks particularly hard, IFR reports, as they have been sourcing as much as a third of their U.S. dollar liquidity in the short-term U.S. market. Citigroup estimates Japanese banks have about $125 billion to $150 billion of CP and CDs maturing before the end of September.

Adding Libor surging insult, to profit-draining NIRP injury (recall that Japanese banks have seen their profits shrink as a result of the BOJ’s recent implementation of negative rates), rising U.S. dollar funding rates pose a further threat to profitability at Japanese banks. Corporate clients are also at risk, as lenders look to pass on the higher costs.

To be sure, some Japanese lenders have been trying to pre-empt the blow from reforms and the Libor blow out. Sumitomo Mitsui Financial Group cut its global CP and CD funding by $7 billion in the year to June, while a $28 billion jump in deposits outpaced a $19 billion increase in lending globally, according to Deutsche Bank. As a result, its loan-to-deposit ratio shrank from 149.6 percent in March 2015 to 135.5 percent at end-June. Mitsubishi UFJ also saw its ratio fall to 115.1 percent from 117.8 percent in March 2015 on the back of a rise in deposits.

In the short term, however, Japanese lenders will be unable to raise enough from deposits to replace the U.S. money markets. Prime money-market funds slashed their holdings of Japanese securities to $115 billion at the end of July, down 25% from $153 billion two months ago, according to ICI. Previously second to only the U.S. by country of issuer, Japan has now fallen to third behind France.

Being increasingly locked out of money markets means that beyond paying up subsantially for U.S. dollars, Japanese banks have few options. Leverage requirements mean global banks are reluctant to provide repos, while foreign-exchange swaps would be a more expensive way to access U.S. dollar funding, said Koichi Sugisaki, a rates strategist at Morgan Stanley MUFG Securities. Three-month CP and CDs now cost roughly 80bp-90bp on an annual basis, but three-month FX forwards have also become more expensive at around 1.5 percent per year, he said.

The surge in Libor, which has also resulted in a spike in the cross-currency basis, has also meant that Japanese buyers are increasingly shying away from US Treasuries which when fully FX hedged no longer generate a notably yield pick up as we reported earlier. - Zerohedge

While the rising rates for Libor are only in their infancy, the direction they are pointing to is eerily similar to 2008 which lead to a liquidity crisis and banks halting their borrowing between institutions. And in an era where debt is so vast that it is impossible to ever pay it off much less pay it down, the die has now been cast as it appears the invisible hand is taking over from the failed policies of the ‘schizophrenic’ central banks.

Kenneth Schortgen Jr is a writer for Secretsofthefed.com, Examiner.com,Roguemoney.net, and To the Death Media, and hosts the popular web blog, The Daily Economist. Ken can also be heard Wednesday afternoons giving an weekly economic report on the Angel Clark radio show.

Don't miss these

- Non Gamstop Casinos UK

- Best Casino Not On Gamstop

- Casino Online Nuovi

- Siti Sicuri Non Aams

- Casinos Not On Gamstop

- Casino Not On Gamstop

- Casino Online Stranieri Non Aams

- Non Gamstop Casino

- Sites Not On Gamstop

- Non Gamstop Casino UK

- Slots Not On Gamstop

- Casino En Ligne

- Casino En Ligne

- Casino En Ligne France

- 信用 できるオンラインカジノ

- UK Casino Not On Gamstop

- Casinos Not On Gamstop

- Casino Online Non Aams

- I Migliori Casino Non Aams

- Siti Casino Online Non Aams

- Non Gamstop Casino Sites UK

- Casino En Ligne Fiable

- UK Online Casinos Not On Gamstop

- Best Non Gamstop Casinos

- Non Gamstop Casino

- Betting Sites UK

- Casino Non Aams

- Crypto Casino

- Meilleur Casino En Ligne Français

- Casinos Belgique

- Casino Online

- Paris Sportif Ufc

- オンラインカジノ 出金早い

- KYC 없는 카지노

- казино онлайн

- Migliori Siti Scommesse

- Casino Online

- Casino En Ligne Fiable

- Casino En Ligne 2026

- Nouveau Casino En Ligne France

- Crypto Casino

- Casino En Ligne

- Migliori Casino Non AAMS

- Siti Casino Non AAMS

- Site De Paris Sportif

- Migliori Casino Non AAMS

- Casino Online Non AAMS

- Migliori Casino Online Non AAMS

- Casino En Ligne Le Plus Payant

- Casino En Ligne

- Meilleur Casino En Ligne France

- Siti Non AAMS

- Casino Esteri Online

- Casino Aams Nuovi

- Casino En Ligne Argent Réel

- Casino En Ligne Le Plus Payant