It has been about 30 years, and perhaps going back to the 1987 stock market crash since the Federal Reserve has been a point of debate during a Presidential race. But in 2016, and at a time when the credibility of the central bank is being questioned from economists and even the business media, Donald Trump is sensing blood in the water and last week decided to put the Fed on trial for the American people to vote for or against in this year’s Presidential election.

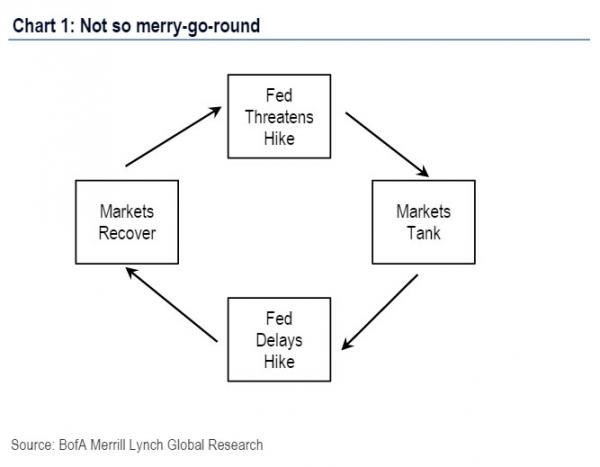

The Fed last year publicly stated that it was time to raise rates for the first time in a decade after continuously decrying that the economy was in recovery, and that their data dependence regarding jobs and inflation were well under their chosen benchmarks. But after a minuscule hike of just a quarter point last December led to a two month smash in the stock markets, the Fed backtracked over the following nine months and has become disconnected in their messages with some Fed Presidents saying a hike was imminent, while in the end Janet Yellen did nothing.

What Trump knows is that the Federal Reserve, the most powerful central bank in the world, since inception was to be autonomous and separate from the political transgressions of Washington.

Historically, the White House and presidential politics, let alone candidates, commenting on interest rates, monetary policy and items related to the Fed mandate was a “hands off” area. This norm seems to have hit deaf ears with the GOP candidate.

Trump appears to now be taking on the Federal Reserve and interest rate speculation.

Only days after his commentary, Trump doubled down on his prior commentary saying, “She’s keeping [rates] artificially low to get Obama retired” He then expanded on Yellen’s actions personally stating, “Watch what is going to happen afterwards. It is a very serious problem… and to a certain extent, I think she should be ashamed of herself.” - Daily Reckoning

The reality is that the Fed has long since abandoned their original mandates and have become the overseer of all monetary and fiscal policies. In fact, both Ben Bernanke and Janet Yellen have spoken on more than one occasion that their job is not only to deal with inflation and unemployment, but to also protect stock markets and foreign banks from their own mistakes and corruptions.

Congress to Yellen:

ROYCE: I’m worried that the Federal Reserve has created a third pillar of monetary policy, that of a stable and rising stock market. And I say that because then-Chairman Bernanke, when he appeared here, stated repeatedly that, “the goal of QE was to increase asset prices like the stock market to create a wealth effect.” That seems as though that was goal. It would stand to reason then that in deciding to raise rates and reduce the Fed’s QE balance sheet standing at a still record $4.5 trillion, one would have to be prepared to accept the opposite result, a declining stock market and a slight deflation of the asset bubble that QE created. Yet, every time in the past three years when there has been a hint of raising rates and the stock market has declined accordingly, the Fed has cited stock market volatility as one of the reasons to stay the course and hold rates at zero. So indeed, the Fed has backed away so many times from rate normalization that - and I think this is a conceptual problem here that the market now expects stock market volatility to diminish the odds of a rate increase. So Madame Chair, is having a stable and rising stock market a third pillar or the Federal Reserve’s monetary policy if I go back to what I originally heard Ben Bernanke articulate? - Zerohedge

Bernanke supplying case through QE to foreign banks:

We followed that with more analyses, showing explicitly how the Fed was providing a constant cash injection toforeign banks courtesy of the rate on overnight reserves which is the amount Fed pays to banks that hold reserves with it, as the bulk of reserves continued to end up with foreign banks - a situation set to become a huge political storm some time in 2014-2015 when the IOER has to rise and the Fed is “found” to have injected tens of billions of “interest” not into US banks but in foreign banks operating in the US, and which then can upstream the “profits” to insolvent offshore domiciled holding companies.

This means that, as we expected several months ago, the only recipient of ongoing Fed money printing are not US banks, but foreign banks operating in the US. - Zerohedge

In part, the problem can also be laid at the feet of Congress, who is the primary authority to regulate the Fed. But since 2008, Congress has not only failed in their duties, but in some cases has demanded that the central bank do more than their mandates. But eight years after the Credit Crisis and subsequent Great Recession, the Fed has now reached a point where they are completely out of viable ammunition, and if someone doesn’t reign them in, the consequences could be monetary policies that will change the landscape of banking, finance, and money forever.

Kenneth Schortgen Jr is a writer for Secretsofthefed.com, Examiner.com,Roguemoney.net, and To the Death Media, and hosts the popular web blog, The Daily Economist. Ken can also be heard Wednesday afternoons giving an weekly economic report on the Angel Clark radio show.