Perhaps it is because $247 trillion is just a number too big to contemplate, or that those in charge have an off button perpetually pushed when it comes to accepting the consequences of debt, but going into 2016 this black swan remains a ticking time bomb that can at any time crater the world even more than a conventional world war.

Oh, and by the way… this is just the derivative exposure of U.S. banks alone.

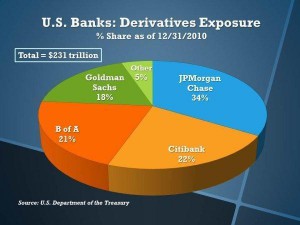

Did you know that there are 5 “too big to fail” banks in the United States that each have exposure to derivatives contracts that is in excess of 30 trillion dollars? Overall, the biggest U.S. banks collectively have more than 247 trillion dollars of exposure to derivatives contracts. That is an amount of money that is more than 13 times the size of the U.S. national debt, and it is a ticking time bomb that could set off financial Armageddon at any moment. Globally, the notional value of all outstanding derivatives contracts is a staggering 552.9 trillion dollars according to the Bank for International Settlements. The bankers assure us that these financial instruments are far less risky than they sound, and that they have spread the risk around enough so that there is no way they could bring the entire system down. But that is the thing about risk – you can try to spread it around as many ways as you can, but you can never eliminate it. And when this derivatives bubble finally implodes, there won’t be enough money on the entire planet to fix it. - Economic Collapse Blog

Global GDP for 2015 fell almost $4 trillion from its 2014 levels to end the year at an estimated number of $73.5 trillion. And this means it would take almost 8 years of using every dollar of production just to cover the derivative bets that historically were an important factor in bringing about the Great Depression of the 1930’s.

In a chapter from The Great Crash, 1929 titled “In Goldman Sachs We Trust,” the famed economist John Kenneth Galbraith held up the Blue Ridge and Shenandoah trusts as classic examples of the insanity of leverage based investment. The trusts, he wrote, were a major cause of the market’s historic crash; in today’s dollars, the losses the bank suffered totaled $475 billion. “It is difficult not to marvel at the imagination which was implicit in this gargantuan insanity,” Galbraith observed, sounding like Keith Olbermann in an ascot. “If there must be madness, something may be said for having it on a heroic scale.” - Rolling Stone

Shenandoah Trust, which was created by Goldman Sachs, was the first use of derivatives.

However, unlike the last market crash just seven years ago, this one will not see taxpayers or governments intervene to bail out the banks, and stave off their insolvencies. Instead, it will be you, me, and all those with money in bank and brokerage accounts who will be stuck with the bill, and beginning tomorrow, Jan. 1, that scenario, especially in Europe, is all but assured.

If you have a bank account anywhere in Europe, you need to read this article. On January 1st, 2016, a new bail-in system will go into effect for all European banks. This new system is based on the Cyprus bank bail-ins that we witnessed a few years ago. If you will remember, money was grabbed from anyone that had more than 100,000 euros in their bank accounts in order to bail out the banks. Now the exact same principles that were used in Cyprus are going to apply to all of Europe. And with the entire global financial system teetering on the brink of chaos, that is not good news for those that have large amounts of money stashed in shaky European banks.

Below, I have shared part of an announcement about this new bail-in system that comes directly from the official website of the European Parliament. I want you to notice that they explicitly say that “unsecured depositors would be affected last”. What they really mean is that any time a bank in Europe fails, they are going to come after private bank accounts once the shareholders and bond holders have been wiped out. So if you have more than 100,000 euros in a European bank right now, you are potentially on the hook when that bank goes under…

The directive establishes a bail-in system which will ensure that taxpayers will be last in the line to the pay the bills of a struggling bank. In a bail-in, creditors, according to a pre-defined hierarchy, forfeit some or all of their holdings to keep the bank alive. The bail-in system will apply from 1 January 2016.

The bail-in tool set out in the directive would require shareholders and bond holders to take the first big hits.Unsecured depositors (over €100,000) would be affected last, in many cases even after the bank-financed resolution fund and the national deposit guarantee fund in the country where it is located have stepped in to help stabilise the bank. Smaller depositors would in any case be explicitly excluded from any bail-in. - Economic Collapse Blog

And sadly for those in the U.S., we already have our own bail-in procedure as proscribed under the 2010 Dodd-Frank Banking Reform Act.

So, the pieces are already in place, and the game is reaching its final gambit. And with oil prices and junk bond failures signalling a massive new liquidity crisis already on the horizon, the potential for these scenarios to take place are growing by the day, and just like in 2008, it will not be the banks who go insolvent or bankrupt, but instead it will be you and me.

Kenneth Schortgen Jr is a writer for Secretsofthefed.com, Examiner.com, Roguemoney.net, and To the Death Media, and hosts the popular web blog, The Daily Economist. Ken can also be heard Wednesday afternoons giving an weekly economic report on the Angel Clark radio show.

Don't miss these

- Non Gamstop Casinos UK

- Best Casino Not On Gamstop

- Casino Online Nuovi

- Siti Sicuri Non Aams

- Casinos Not On Gamstop

- Casino Not On Gamstop

- Casino Online Stranieri Non Aams

- Non Gamstop Casino

- Sites Not On Gamstop

- Non Gamstop Casino UK

- Slots Not On Gamstop

- Casino En Ligne

- Casino En Ligne

- Casino En Ligne France

- 信用 できるオンラインカジノ

- UK Casino Not On Gamstop

- Casinos Not On Gamstop

- Casino Online Non Aams

- I Migliori Casino Non Aams

- Siti Casino Online Non Aams

- Non Gamstop Casino Sites UK

- Casino En Ligne Fiable

- UK Online Casinos Not On Gamstop

- Best Non Gamstop Casinos

- Non Gamstop Casino

- Betting Sites UK

- Casino Non Aams

- Crypto Casino

- Meilleur Casino En Ligne Français

- Casinos Belgique

- Casino Online

- Paris Sportif Ufc

- オンラインカジノ 出金早い

- KYC 없는 카지노

- казино онлайн

- Migliori Siti Scommesse

- Casino Online

- Casino En Ligne Fiable

- Casino En Ligne 2026

- Nouveau Casino En Ligne France

- Crypto Casino

- Casino En Ligne

- Migliori Casino Non AAMS

- Siti Casino Non AAMS

- Site De Paris Sportif

- Casino Online Non AAMS

- Migliori Casino Non AAMS

- Casino Online Non AAMS

- Migliori Casino Online Non AAMS

- Casino En Ligne Le Plus Payant

- Casino En Ligne

- Meilleur Casino En Ligne France

- Siti Non AAMS

- Casino Esteri Online

- Casino Aams Nuovi

- Casino En Ligne Argent Réel

- Casino En Ligne Le Plus Payant

- Poker Online Migliori Siti

- Siti Poker Online

- Giochi Senza AAMS

- Slots Non AAMS

- Siti Non Aams

- Casino Non Aams